Contributed By –

Site Selection for New and Relocated Branches

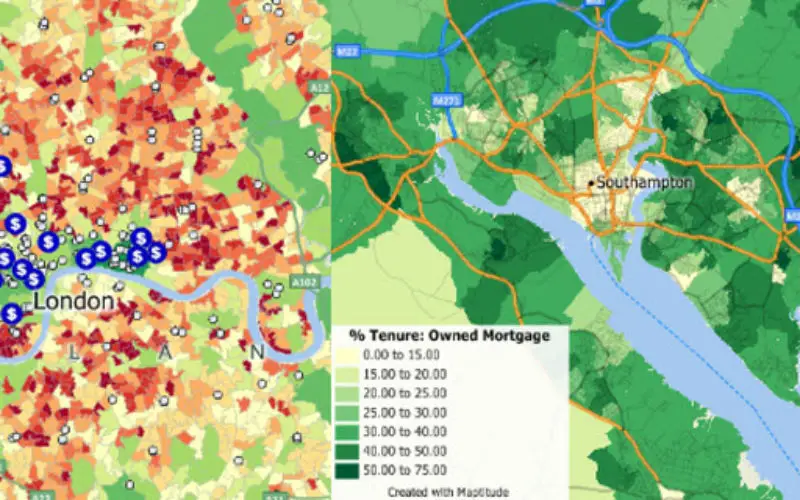

It’s not difficult to comprehend the basic idea of depicting market statistics on maps in an effort to evaluate locations. But these days, there are so many more techniques and tools in the arsenal to allow the organization to go so much further. “Spatial interaction modelling” captures the patterns of customer locations in relation to the branches they may choose to execute transactions. Systems can go to work calculating complicated geography-based statistics (e.g. households within a 5-minute drive, an index representing overall competitive intensity that takes into account proximity of branches, whether or not a branch is on the “going home side” of the street for commuters, etc.) for thousands of locations at one time. Distribution of customer home locations can be fully analyzed to better understand impacts on nearby branch openings.

Besides assessing a given site opportunity, GIS helps prioritize alternative site locations, assess the expected performance of existing branches based on the market conditions faced, quantify the estimated financial impact of changes to the branch network (including competitors’), evaluate stores in which a small banking kiosk may be installed and assess branch relocation opportunities to name a few.

Branch Closure Evaluation

Assessing the attractiveness of the markets in which branches operate with the help of GIS can help a bank decide whether or not to reduce its presence in that market and assess the risks in doing so? But GIS-based analysis of closure opportunities is especially helpful when it comes to predicting the customer loss (churn) result should a given branch be closed. Capturing this ability to retain customers through transfer of business to nearby branches can have a very significant impact on the decision involved, where it’s sometimes better to close one branch that performs on its own better than another candidate for closure. Some banking organizations are taking this concept to the next level and applying sophisticated customer churn models across a national network of branch locations in an effort to identify consolidation opportunities.

Targeted Marketing Campaign Enhancement

Using GIS, neighborhoods, ZIP/postal codes, or individual addresses can be assessed as to whether or not they meet certain geographic and/or demographic criteria and can be scored or ranked according to the corresponding potential to respond to campaigns. For example, rather than mailing a letter randomly to customers with certain cities, one can identify postal codes that are within a 10 minute drive of one of the organization’s branches and are in neighborhoods with an average annual household income of at least Rs. 50,000 to name one example.

Resource Allocation

When it comes to increasing staff, merely waiting to first see that a branch has clearly become too busy can mean significant business lost. One branch operating at capacity may already be capturing virtually all of the business it can expect based on the market conditions it faces while another experiencing the same customer wait times may have many more customers turning away due to those waits. By analyzing markets correctly, the bank can better anticipate expected business volumes and the need for more staff before the branch becomes too busy.

A similar analysis of branch locations in related to market potential can be especially beneficial when an entirely new service and corresponding new staff are being introduced or certain types of staff are only being deployed in selected branches. In these cases, GIS-based market analysis may hold critical information when information about existing customers doesn’t provide all the answers.

Another of many examples in this category is the setting of optimal hours of service across branches. The location positioning of the organization’s branches in relation to the hours of service offered at nearby competing branches may, for example, play a big role in determining what’s appropriate.

Market Profiling

Even if no changes to the branch network or major marketing campaigns are involved, simply knowing the regions served (such as demographic characteristics) can go a long way toward helping branches fine-tune appropriate service processes and tailor local marketing efforts. Defining primary trade areas through GIS deployment is a big part of this effort, where geographic positions are determined for customers and processed to identify such regions. Once in hand, the trade areas can be used to identify differences between any demographic information the organization already has for its customers and the prevailing demographics in the regions themselves. This may reveal, for example, a higher than expected proportion of the

Customer Relationship Management (CRM) Support

In cases where important demographic information is unavailable for customers, GIS can be used to attach neighborhood-level demographic averages as a way to effectively either summarize characteristics of customers as groups or predict the likelihood of customers having certain demographic attributes. This in turn can be incorporated into tools used to manage interactions with customers or into various analyses performed for CRM purposes (models predicting customer behaviors, development of customer segmentation systems, etc.). As a completely different example, proximity to branches can be almost instantly provided to a potential commercial customer who needs to have good access to on-site banking from its own network of business locations.

Merger and Acquisition Evaluation

By analyzing the location pattern of branches of an acquisition candidate, for example, a bank can determine the overall “geographic fit” in relation to its own branch network. For instance, it may be ideal that the other bank’s branches are either almost immediately adjacent to its own or sufficiently removed from them yet serving markets that are similar or otherwise sufficiently attractive. GIS can help quantify the degree to which this holds true.

In other cases, such as a major merger between banking organizations, there are certain processes used by governmental agencies to help them determine whether or not a merger will leave the organizations with too much dominance in certain markets (and thus unfairly set fees, as one of many examples). This kind of review process has a key geographic element to it. By using GIS, banks can actually perform a similar “self-assessments” to allow them to anticipate and potentially address these issues in advance of governmental reviews.

Customer Navigation

Branch locators are one of the more recognized applications of GIS for bank branches these days. But some banks are going further than others in this capacity. The effectiveness of a branch locator depends on several factors:

The flexibility in how customers can specify locations for searches

- The amount of branch information made available (including photos)

- How current the data is maintained

- The degree to which the look is tailored to the bank’s brand image

- The range of criteria that can be specified for searches (e.g. nearest branch offering X, Y, and Z)

- The visual quality of the maps

- The accuracy of the branch positions

- The proportion of searched locations that are successfully found

- The speed in which information is returned

- The capacity of the system (speed as many customers use it at the same time)

Beyond helping customers navigate, some banks provide expanded versions of these store locators for internal use across the organization, where much more confidential branch information can be incorporated.

“Location based services” (LBS) also represent applications of GIS related to this category. The term is a complex one that has been described differently by different parties over the years, but can be characterized as information services supplied over mobile devices (such as smart cellular phones) that incorporate the geographic location of the mobile devices. For banks, the examples may include pushing out advertising to subscribing customers that are within close proximity to a branch, simply providing the above branch locating support using

Performance Management

In many ways, the geographic positioning of a bank’s branches and offices in relation to market conditions determines its business potential (the financial performance it should expect accordingly) and GIS helps banks do this at both the local branch level and at regional levels.

Predictive models of branch performance, based in large part on analysis and visualization provided by GIS, define how well a branch should be performing (revenue generated, funds under management, customers booked). As a result, branch managers and other key staff can be more accurately evaluated beyond the actual financial results themselves for a given branch.

The same kind of concept applies in determining the effectiveness of new products and services, where new customers can be plotted in relation to other market data to estimate penetration levels. The bank may find that the success of such new offerings depends in part on selected geographic patterns and demographic attributes of markets.

Enhancement to Executive Information Systems, Reports, and Presentations

In many ways, GIS provides key contributions to better use of corporate information systems for decision-making purposes. Credit-card-only customers and those otherwise not connected directly to a bank branch can be assigned to branches based on proximity so that this customer data can be integrated with other data at a branch level and at levels representing formal organizational groupings of branches. The appropriate groupings themselves can be determined or redefined based on GIS analysis. The concept of “geo-accounting” in general is enabled, where financial data is allocated to locations and standardized market boundaries where possible to allow review and extraction of data by geography versus merely the internal accounting organization.

Maps depicting metrics as charts or regional colouring can be incorporated into business intelligence systems to allow more effective display of tabular data. And finally, new KPIs (key performance indicators) can be defined for dashboards such as estimated market share.

In almost all cases, one can substitute “branch” with “store”, “restaurant”, “café”, or “dealership” and the applications apply almost equally to the respective industry.

Online tracking of Cash status in ATM’s

Distribution and replenishment of the Cash to the ATM according to demand and in-time is a major challenge in the area of ATM management as the dead-cash results into substantial interest loss.

GIS based Real Time solution for the replenishment and management of ATMs provides highly effective approach to the cash management cycle. “Auto detect” component provides real time data in order to optimize the servicing of ATMs, “just in time”, based on actual customer demand. This solution should be a flexible, dynamic model, which operates in real time and is based on actual customer needs to improve the servicing of ATMs, resulting in improved efficiency and reduced costs.

GIS based solution displays the ATMs on the map along with the cash status to help in better visualization and better optimization in Cash distribution. Cash requirement for each day for a Bank/ATM can be predicted with the help of the history of cash transactions over a certain period during previous years and also with the help of Demographic data such as population density, Socio economic information etc.

Competitor Analysis

This analysis answers the queries, where are our competitors located? This analysis identifies the competitors and their customers on the Map, analyze the reason for existing performance.

Re-finance services

Banks may do their marketing program for their products such as re-finance mortgage. Using GIS banks can deliver awareness to potential customer with minimal cost and target their most desirable customers.

For example, by plotting existing customer on the map and using content to get property transacted value and Property Asking Value to decide whether to advise customer to refinance the mortgage loan. With the information available and content, Banks can precisely target customer with marketing campaign and thus, bring low risk to decision. For this case, if target customer agreed to have re-finance their mortgage loan, additional value (Current loan – property transacted value) will be additional revenue for the bank.